From Confidentiality to Compliance: New Insurance Agent Rules Explained

Kathmandu — Nepal Insurance Authority has issued the Insurance Agent Directive 2026. The directive has been introduced under Section 166 of the Insurance Act 2022 to make the functioning of insurance agents more systematic, professional, transparent, and accountable.

Under the directive, certain individuals have been deemed ineligible to become insurance agents. As per Rule 42, those who do not meet qualification requirements, are declared insolvent under prevailing laws, are blacklisted and have not completed one year since removal from the blacklist, have conflicts of interest with insurers, or, in the case of institutional agents, have not cleared taxes or have unaudited financial statements, are barred from becoming agents.

To strengthen professional capacity in the insurance sector, each insurer is required to provide at least 15 hours of professional development training to agents during each renewal period. The training must cover technical aspects of insurance, legal provisions, and market conduct.

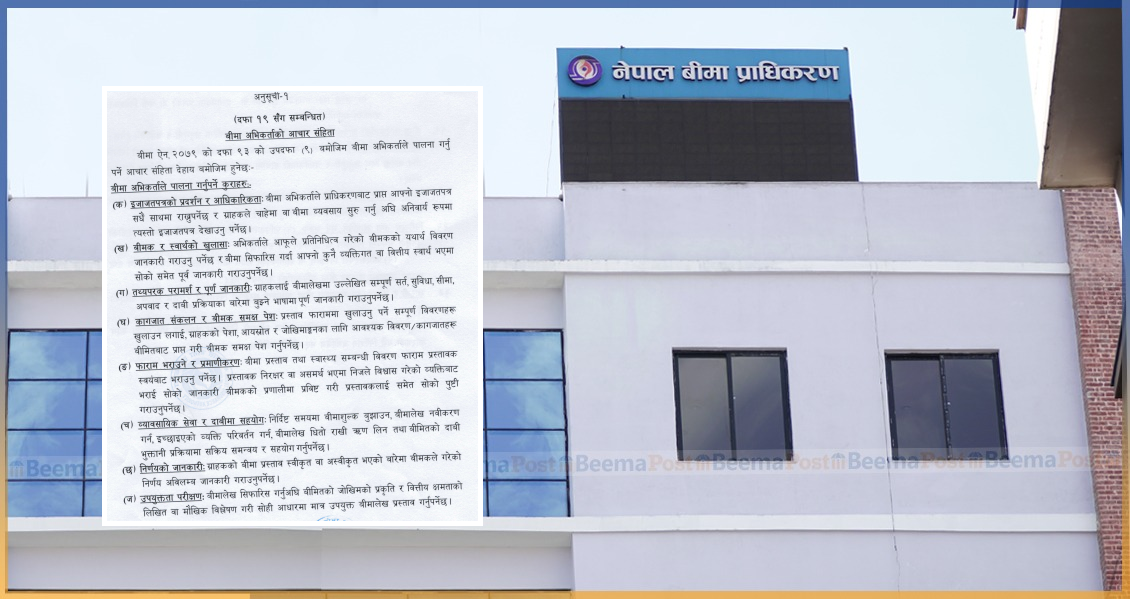

According to provisions on duties, responsibilities, and rights, agents must carry their license issued by the authority at all times and present it when required. While conducting insurance business on behalf of insurers, they must follow fundamental principles and clearly explain all policy terms, benefits, and claim procedures to clients in simple and understandable language.

Agents are also required to provide accurate information about the financial condition of the insurer upon request, assist clients in properly filling out proposal forms, collect necessary documents and submit them to the insurer, and play a coordinating role in policy renewal and claims processing. Policies must be recommended based on the client’s risk profile, financial capacity, and actual needs.

The directive strictly defines a code of conduct for agents. They must always carry their license, disclose any conflicts of interest, provide complete and truthful information to clients, and maintain confidentiality.

Agents are prohibited from falsifying or concealing client documents, and proposal forms must be filled out by the clients themselves. They are also required to actively assist in renewals, premium payments, loan facilities, and claims procedures.

Prohibited activities include engaging in unfair competition, offering commission rebates or gifts as inducements, operating without a license, breaching client confidentiality, coercion or misconduct, obtaining undue financial benefits, performing dual roles, violating rates and terms, spreading misleading information, and committing fraud or forgery.